This theme on Africa’s Energy Futures explores the challenges and strategies for Africa’s transition to renewable energy and the energy requirements for more rapid but sustainable development. It complements the theme on Africa’s Climate Futures and, given the close link between energy and climate change, we use the same scenarios in these two themes. For more information about the International Futures modelling platform we use for our scenarios, please see About this Site.

Summary

We begin this theme by discussing the critical role of energy in human development and provide a brief history of energy production and demand. We then provide a concise overview of the current energy landscape, globally and for Africa.

Next, we analyse the likely energy supply and demand forecast to 2050 and sometimes 2063. We differentiate between six energy types: oil, gas, coal, nuclear, hydroelectric, and other renewables. This analysis is grounded in the Current Path forecast, which assumes continuity in Africa’s current developmental trajectory without major shocks.

Energy production across these categories is quantified in barrels of oil equivalent (BOE) and millions or billions of barrels of oil equivalent (MBOE or BBOE), facilitating a direct comparison among them. These initial sections project the future evolution of energy trends up to 2050, aligning with global goals like ‘achieving net zero by 2050’, and extend our outlook to 2063 to coincide with the African Union’s Agenda 2063 vision.

Moving beyond the Current Path, we address the necessity of establishing fossil energy production limits to align with the 1.5°C global warming target set by the Paris Agreement amidst a growing scientific consensus that anticipates a 2°C warming scenario.

We examine a suite of policies for Africa to reduce fossil fuel use, ramp up other types of energy production and reduce carbon emissions. This involves reviewing the effects of strategies proposed by the UN Environment Programme (UNEP) and other entities to significantly cut coal use and reduce oil and gas production worldwide.

The subsequent Africa Energy Policy scenario examines the ramifications of diminishing coal and oil production without limiting gas. Our analysis indicates that constraints on gas production would create an unmanageable energy production shortfall for a continent still with very low levels of energy availability.

The scenario includes various mitigation efforts and the expansion in renewables, hydro, and nuclear power needed to bridge the remaining energy demand gap. The scenario also incorporates carbon sequestration and enhanced energy efficiency measures to gauge their impact on carbon emissions.

We then apply the Africa Energy Policy scenario to the Combined Agenda 2063 scenario, where Africa realises its socio-economic and governance potential and achieves rapid growth. This Sustainable Africa scenariorepresents an ambitious vision for Africa’s sustainable development and energy transition, aiming for a more prosperous and less carbon-intensive future.

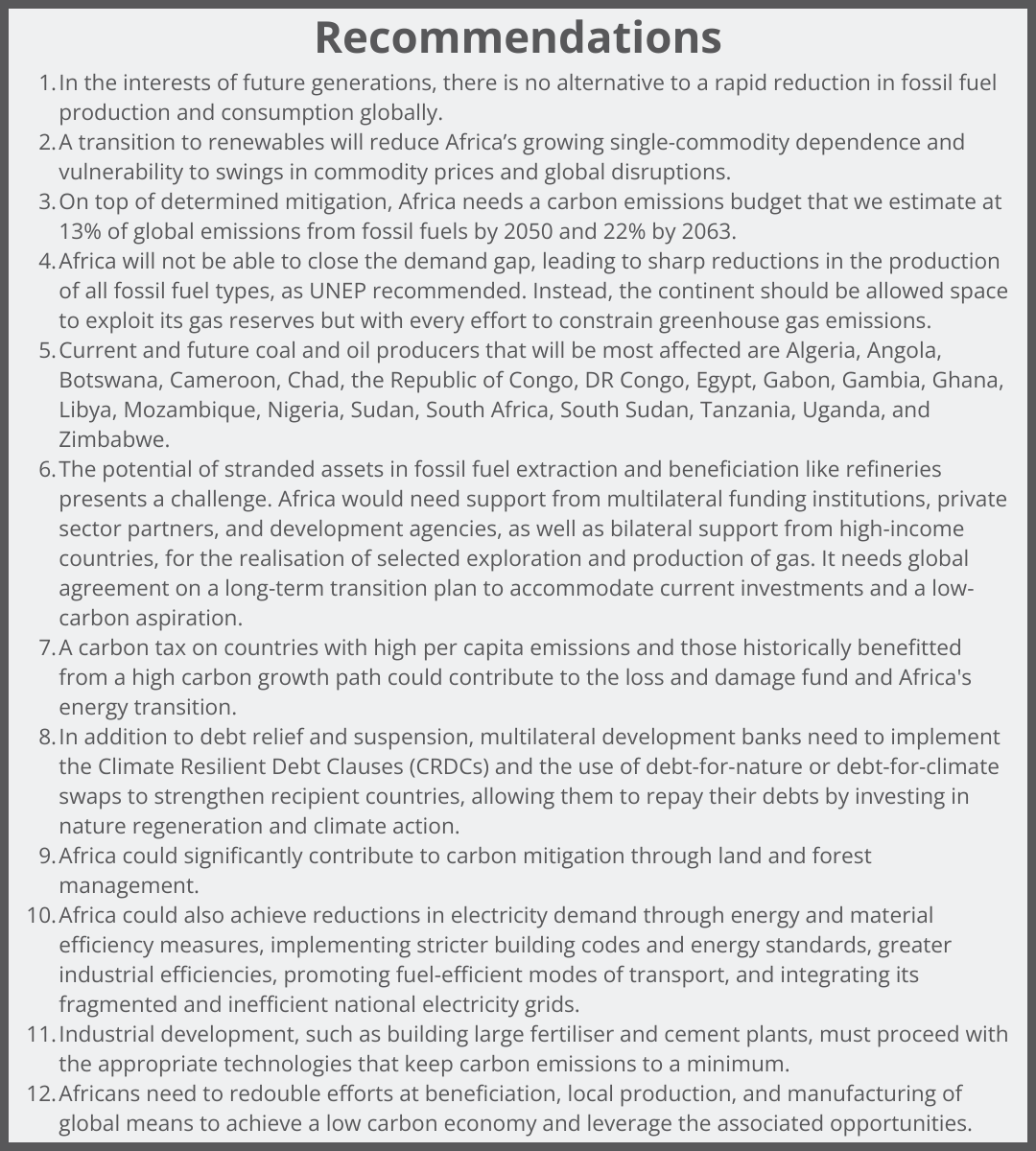

A summarising conclusion includes key recommendations for decision-making. It will not be possible to close the 5.9 BBOE production gap that will be left with the ending of coal production by 2040 and a drastic reduction in oil and gas by 2050 as recommended by UNEP. Instead, Africa would need to be provided with room to exploit its gas endowment with due consideration of the challenge of stranded assets. We list the African coal and oil producing countries that will be most affected with the recommended production reductions. We point to the need for a differentiated global carbon tax, and the support that Africa would need from multilateral funding institutions, private sector partners in the West, development agencies and bilateral support from high-income countries for the realisation of a viable carbon emissions pathway, including for selected exploration and production of gas.

In addition to renewables, Africa will need significant amounts of nuclear energy, more hydro and invest in energy storage. Currently small and modular nuclear energy reactors offer the most viable technology to close a large portion of Africa’s base-load energy demand.

In addition to debt relief and suspension, multilateral development banks need to implement the Climate Resilient Debt Clauses (CRDCs) developed in response to the Sustainable Debt Coalition created at COP27 in Egypt and the use of debt-for-nature or debt-for-climate swaps to strengthen recipient countries. Much more attention must also be paid to repurposing solid waste and efforts towards the circular economy. Finally, knowledge transfer and domestic investment in exchange for the export of beneficiated raw materials should be front and centre in an African strategy to leverage the associated opportunities.

All charts for Theme 15

Introduction: Energy and Sustainable Development

Energy is essential for economic growth and human progress. The relationship between per capita energy consumption and various development indicators such as access to food, wealth, health, nutrition, clean water, infrastructure, education, infant mortality and life expectancy is powerful, particularly at low levels of development. Thus, low scores on the Human Development Index (HDI) correlate with low per capita energy use.

The HDI finds that with sufficient energy, development can be rapid, especially at low-income levels and posits a requirement of 8.62 barrels of oil equivalent (BOE, equivalent to 100 gigajoule) per person to allow for rapid development. At this level small increment of energy use corresponds with a relatively large increase in HDI. Diminishing returns become evident at higher levels of use and, above16.34 BOE, there is no statistical significant relationship as a saturation effect sets in.

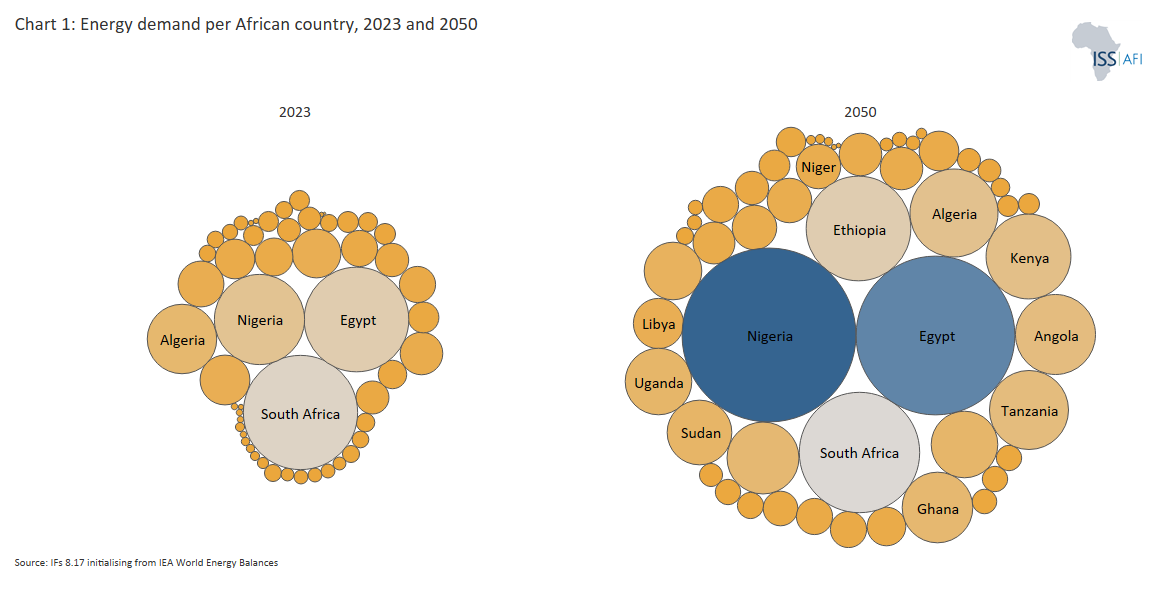

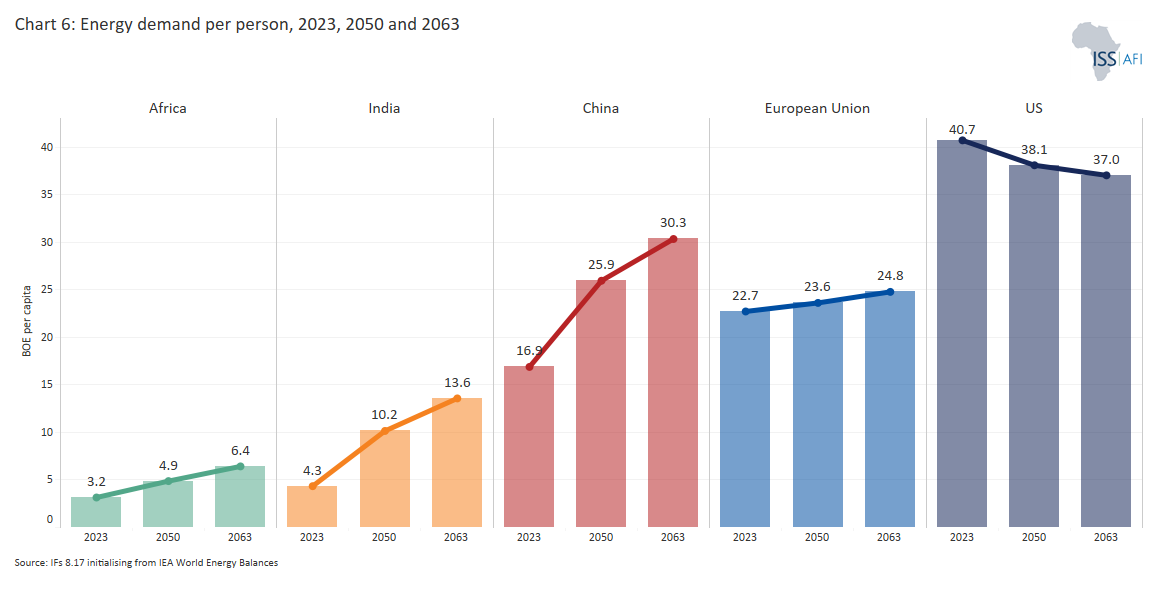

In light of this, Africa has an energy mountain to climb. Only six African countries (Libya, Mauritius, South Africa, Seychelles, Botswana and Namibia) have per capita demand above the threshold of 8.62 BOE in 2023, which is required for rapid human development gains. The average energy demand per person in Africa in 2023 is much lower at 3.2 BOE and will only modestly increase to 6.4 BOE by 2063 on the Current Path forecast. Thus it is no surprise that in a high growth scenario (the Combined Agenda 2063 scenario) modelled elsewhere on this site, Africa’s energy demand is almost 40% above the 2050 Current Path forecast and energy demand per capita is significantly higher. Chart 1 presents current and future energy demand per African country, and Chart 6 presents energy demand per person.

Rapid development in Africa will be associated with large increases in energy demand and associated carbon emissions should the continent proceed on the same fossil fuel development pathway as today’s developed economies.

At higher levels of development, technology can allow energy use per person to decline even as incomes increase. The energy required for human development in high-income countries has therefore decreased over time. In 1975, high human development characterised by a long and healthy life, a well-educated population, stability, and a decent standard of living, needed 16.3 BOE per person. This had almost halved to 9.8 BOE by 2005. Yet, total energy demand continues to grow globally due to population growth and the development demands in low and middle-income countries. Looking long-term, the energy demand from data centres, artificial intelligence, and cryptocurrency may slow energy reductions in many high-income countries and is expected to double from 2% of global demand in 2022 by 2026.

The trend of increased energy demand associated with development is evident when considering the Current Path forecast. For a world population that will increase from 8 billion in 2023 to 9.8 billion in 2050 (i.e. by 21%), energy demand[1] will increase from 94.2 billion barrels of oil equivalent (BBOE) to 134.8 BBOE. This represents more than double the rise in population at 43%, reaffirming the strong relationship between energy and development.

The relationship between energy and development at higher consumption levels is complex because other factors, such as the economy’s structure (including, for example, the size of the manufacturing sector), institutional quality and social capital, become more important to improve human development. The result is large differences in energy consumption amongst high-income countries at roughly the same levels of development, such as the US, which uses significantly more energy per person compared to Norway or Sweden.

Energy: A Brief History

Over time, the source from which we get our energy has changed. Until the mid-19th century, most energy came from traditional biomass – burning wood, crop waste, or charcoal. With the Industrial Revolution came the rise of peat, coal and, later, oil and gas. Hydropower gained momentum at the turn of the 20th century. China is the leader in hydropower globally, generating four times more than Canada and Brazil, ranked second and third.

Then, from the 1960s, more countries embarked on using nuclear power. Today, the United States, France, and China have the largest installed nuclear power capacity. Renewable energy sources, solar and wind, only emerged in the 1980s, now driven by the imperatives to curb global warming and climate change.

Among the three sources of fossil fuels, coal has the largest carbon emissions. Natural gas produces lower carbon emissions and air pollution than coal and oil but releases methane (a potent greenhouse gas) and other non-CO2 pollutants. In 2021, natural gas production accounted for 40 million tons of methane emissions, roughly equivalent to the methane emissions generated by the entire oil industry. As outlined by the International Energy Agency (IEA), coal contributed almost 44% of global carbon emissions from fuel combustion in 2021, closely following oil at 32% and natural gas at 22%.

In its ‘Renewables 2023’ report, the IEA states that 507 gigawatts (GW) of renewable energy capacity was installed globally in 2022, increasing the installed base to about 3 600 GW, with solar photovoltaic (PV) accounting for three-quarters of worldwide additions.

In 2023, China extended its position as a global renewables frontrunner by surpassing the collective 2022 solar PV installations of the rest of the world. Furthermore, there was a notable increase of 66% in China’s wind power additions from 2022 to 2023. As a result, China is likely to achieve its 2030 target for wind and solar PV installations in 2024, six years ahead of schedule.

According to the IEA[2], a powerful alignment of costs, climate and energy security goals plus industrial strategies such as the 2022 US Inflation Reduction Act means that clean energy investment is now rising much faster than investments in fossil fuels.[3] Investment in global exploration and production (upstream oil and gas investment) has slowed but steadily declined for several years. Russia’s invasion of Ukraine temporarily increased oil and gas demand as European countries scrambled for alternative sources from Russia, but prices have subsequently stabilised.

Many challenges remain. The use of solid fuels (biomass, coal and charcoal) as a household energy source, is still common for more than 3 billion people globally. However, it has declined with more citizens accessing electricity to cook, heat and cool. Many of these households are in Africa, such as Ethiopia, the DR Congo, Tanzania, Nigeria and Mozambique, where most citizens in rural areas continue to use traditional biomass for cooking and heating. Solid fuel use, particularly indoors, is associated with increased mortality[4] from pneumonia and other acute lower respiratory diseases among children, as well as increased mortality from chronic obstructive pulmonary disease, cerebrovascular and ischaemic heart diseases, and lung cancer among adults. Because solid fuels generate household air pollution, it is associated with more than 2 million deaths in 2019.

In contrast, in more advanced economies, biomass is used at household, municipal, and industrial levels to produce energy as part of a transition to renewables, illustrating energy’s evolution and technology’s role in the modern world. In tomorrow’s economy, biomass, solar and wind offer the prospects of energy independence at the household level and possibly the development of a circular economy where households, businesses and communities generate their energy, food and water as part of their waste and garbage management processes.

Biomass is typically produced and consumed near the end-user, likely within the same country, village or community. Coal, oil, gas, hydrogen and electricity can be transported between countries by rail, road or sea, gridlines or pipelines, meaning that these sources and types of energy that are mined or produced in one country can satisfy demand in another. The result is a complex system in which energy sources are connected and transported across national boundaries either in unrefined or final form. Production in one country feeds demand in another.

At a sufficient scale, fossil fuel, hydrogen and electricity producers can exert significant influence. For example, for several decades towards the end of the 20th century, large energy producers, mostly in the Middle East, established a cartel, the Organization of the Petroleum Exporting Countries (OPEC), that effectively controlled petroleum prices globally. OPEC market dominance was subsequently disrupted, particularly by large-scale oil and gas fracking in the US, to the extent that, together with an increase in energy efficiency and renewable energy, the US has emerged as the largest oil and gas producer globally. It became almost energy-independent, even preparing to export large amounts of natural gas to others. Today, China, too, is actively pursuing energy self-sufficiency but has yet to satisfy domestic demand from own national resources and has replaced the US as the largest market for oil and gas with sources from the Middle East.

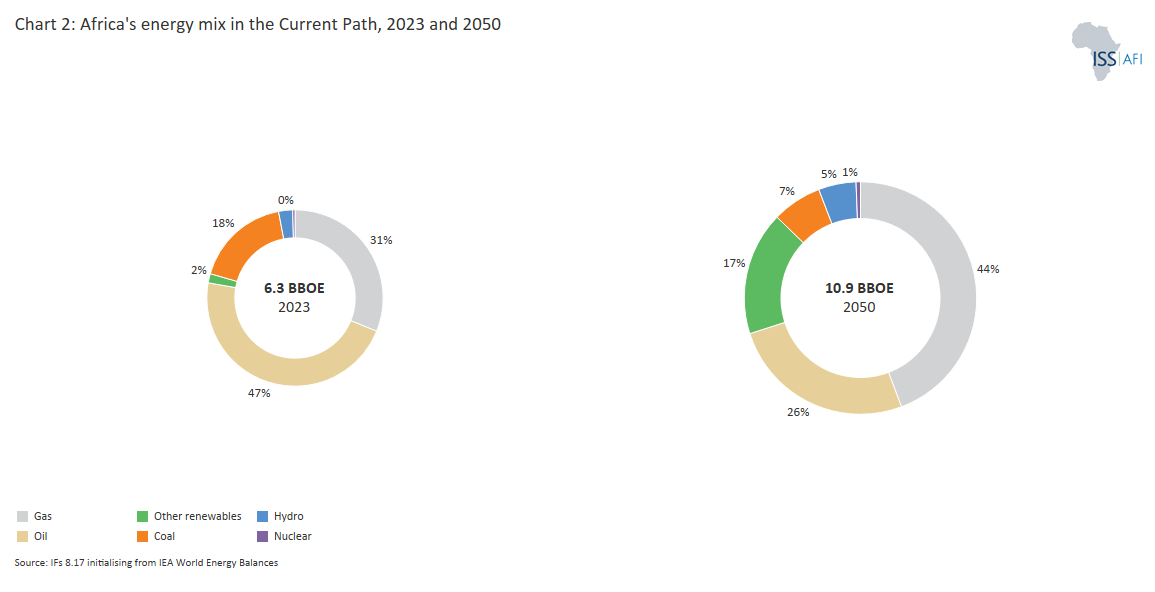

Using a common yardstick to measure energy production, in this instance BBOE, only about 4.8% of the global energy production came from ‘other renewables’, mainly sun and wind (equivalent to 4.6 BBOE) in 2023. The share from oil was at 31%, gas at 27%, coal at 29%, and the remainder from nuclear (5.4%) and hydro (2.9%). The share of oil, coal, and gas production, the three components of fossil energy in the global energy mix, has remained above 80% for the last two decades and is declining slowly, with global peak coal production possibly occurring in 2023.

Africa’s Energy Landscape

Africa is experiencing facing a growing addiction to gas and oil. Yet, in 2023, Africa produced only 6.6% of world energy, which would increase to 8.1% in 2050 – a portion vastly out of balance with its large and growing population and development needs.

Energy demand, however, in Africa is less than 5% of the world. The difference between production and demand reflects that the continent has abundant energy resources but exports a significant portion. According to the Climate Action Tracker, around 40% of Africa’s gas production is exported, primarily to Europe, China and India whilst again importing refined products.

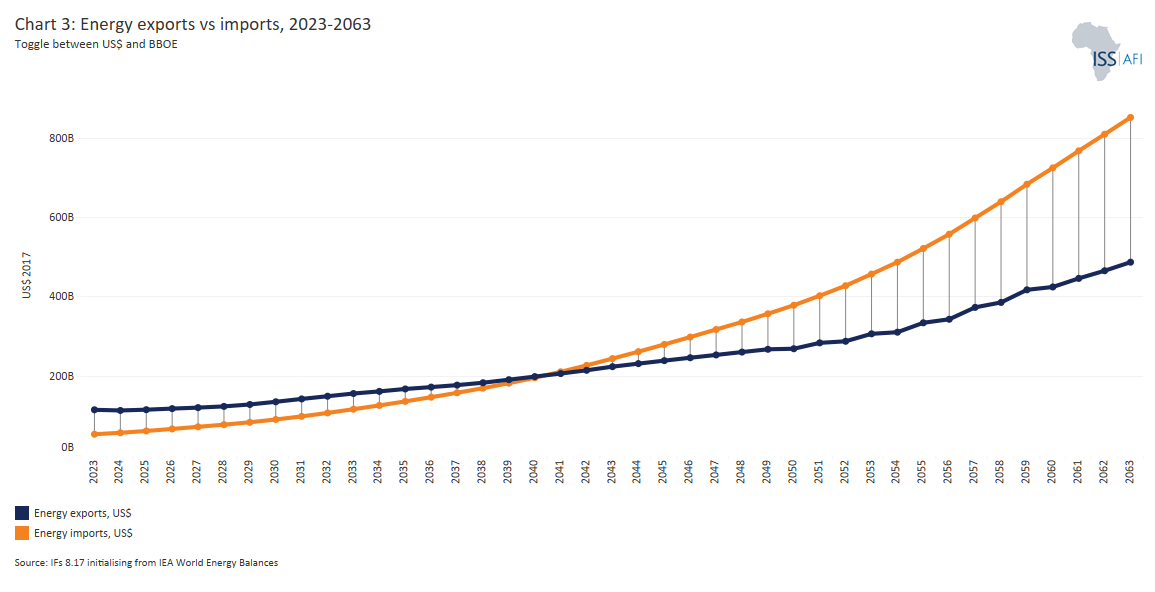

In 2023 (Chart 3), African countries exported more energy to other African countries and the rest of the world than they imported. That year, African countries exported energy equivalent to 67.9% of their domestic energy demand. Rapid population and income growth mean the continent’s energy demand will increase rapidly. From 2041, African countries will collectively import more energy than they import, with large country-to-country differences.

Several African countries are dependent upon energy imports[5] for more than 50% of their domestic demand, ranging from Morocco (for 93% of its demand), Senegal, Benin, Tunisia, Mauritania, Mauritius, Eritrea, Mali, Uganda Togo, Mozambique, Burkina Faso and Namibia (at 50%). By 2050, 29 African countries will import more than 50% of their demand. Being dependent on energy imports makes these countries vulnerable to price fluctuations (such as the effect on gas prices that followed Russia’s invasion of Ukraine) and supply disruptions in international markets (such as the attacks on commercial vehicles in the Red Sea early in 2024). It also points to the large potential with the development of Africa’s five electricity trading entities or pools[6] where demand in one country can be offset by production in another.

Together with its low levels of development, the result of these exports is that Africa’s people are energy-poor. Only 57% of Africa’s population has electricity, meaning 596 million people lack access to the most basic household resource for heating, cooling, cooking, reading and home education. The data highlights the stark contrast between the continent’s energy potential and widespread energy poverty.

In addition to limited access to electricity, a fundamental requirement for a decent quality of life, Africans generally lack energy for transportation, industry, agriculture, construction and services to enable economic growth. This energy paradox is particularly evident in countries such as the Central African Republic, Chad and South Sudan, where abundant energy resources do not translate to electricity access.

Yet Africa has roughly 7.3% of the world’s proven oil reserves[7], approximately 7.7% of the gas reserves[8] and 4.8% of coal, most of the latter in South Africa, which uses coal for much of its electricity and exports large amounts.

Coal production is the third largest energy source produced on the continent (oil and gas are first and second, respectively), but this is narrowly exploited in only a few countries. South Africa hosts 86% of Africa’s entire coal-fired generation capacity. Smaller coal-fire plants are operational in Namibia, Botswana, Zimbabwe, Morocco, Madagascar, Mauritius, Nigeria, Zambia and Senegal.

While the MENA region, including North Africa, holds around 60% of the world’s proven oil reserves, most countries in Sub-Saharan Africa (SSA) import most of their refined fuel requirements from elsewhere. SSA only has 2 to 3% of the world’s refining capacity and is thus vulnerable to oil price shocks and regional fuel shortages. The region relies heavily on liquid fuels for primary energy consumption, particularly diesel, which accounts for most of transportation fuel consumption, baseload, and backup electricity generation. For example, up to 90% of Senegal’s electricity is generated via diesel and heavy fuel oil.

Improving local liquid fuel production is particularly challenging in the region due to underdeveloped infrastructure and unreliable transportation networks. Apart from Kenya and South Africa, which have pipelines to transport liquid fuels, petroleum products are generally transported by road and truck.

Several African countries have expressed interest in building nuclear power stations. Currently, only South Africa has a commercial nuclear power plant, the Koeberg station near Cape Town, that accounts for around 6% of its electricity production, with a capacity of 1 940 MW. The first unit was synchronised to the grid in 1984 and scheduled for decommissioning in 2024, but its lifespan is currently being extended to 2044. In 2021, the National Energy Regulator of South Africa approved plans for South Africa to procure an additional 2 500 MW of nuclear power.

Egypt has embarked upon a nuclear build program and awarded a US$25 billion contract to Russia’s Rosatom company for a 4.8 GW power plant at El-Dabaa along the Mediterranean coast. The first unit should enter service in 2028; all four will be operational by 2030. Other African countries that are exploring nuclear power options include Ghana, Morocco, Uganda, Burkina Faso, Kenya and Rwanda, but none have started construction.

Data on clean energy differs, but Africa boasts 60% of the world’s best solar resources, utilising only 1% of its installed solar PV capacity. It sits on top of numerous active hot spots, offering vast potential for geothermal energy generation.

Large parts of Africa also have excellent wind resources, particularly in coastal areas and the Great Rift Valley.

It is therefore concerning that, in 2023, only 1.7% of Africa’s energy production came from ‘other renewables’ (essentially wind and solar), which is equivalent to 0.1 BBOE. Its energy production landscape is heavily fossil-fuel dependent and is primarily composed of oil at 46.6%, gas at 31.2% and coal at 17.6%.

In addition to its abundant renewable energy resources, Africa has the most significant untapped hydropower potential of any region globally, but hydro only constituted 2.6% of total energy production in 2023[9]. The continent has many rivers and waterfalls, making it a prime candidate for hydropower generation. For example, Ethiopia recently completed the US$5 billion Grand Ethiopian Renaissance Dam (GERD) on the upper reaches of the Blue Nile close to its border with Sudan, the third-largest hydroelectric facility in the world in terms of installed capacity, capable of generating almost 6.5 GW in peak operating conditions. With the completion of GERD, Ethiopia is now the largest source of hydroelectric power in Africa, having overtaken the Democratic Republic of the Congo (DR Congo).

Other hydroelectric projects include the Julius Nyerere Hydropower Plant and Dam in the Rufiji River basin in Tanzania, which would deliver 2.1 GW. In the DR Congo, the first two dams of the Grand Inga scheme, Inga l and ll, are built, and Inga lll is imminent. But the larger Grand Inga (of which Inga lll would only be a first phase) has been in planning since the 1950s, held back by poor planning, inefficiencies, corruption – and the need to lay transmission lines over several thousand kilometres to the large South African and Nigerian markets.

Energy on the Current Path forecast

Energy production to 2063

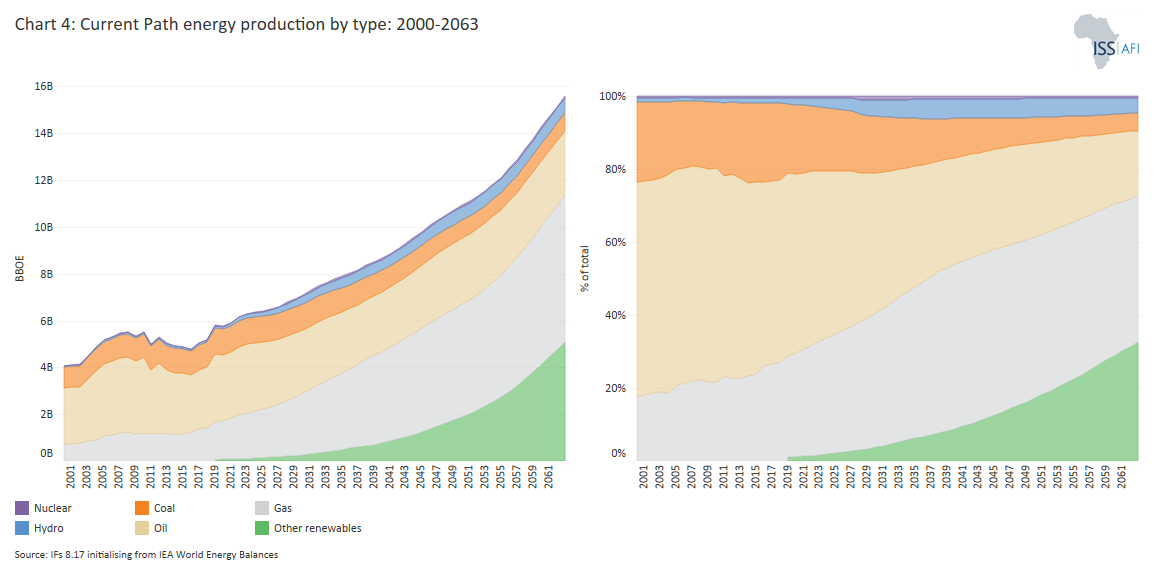

Chart 4 presents a picture of production by energy type since 2000, with the Current Path forecast to 2063. The data in BBOE is available for various global groups, key countries, African regions and all African countries, utilising the drop-down menu. The user can also choose to display production in BBOE or as a per cent of the total.

In this forecast, global gas production overtakes coal production in 2026 and oil in 2031. Globally gas production steadily increases until reaching a plateau in 2046, followed by a slow decline. At the global level, the combined energy production from solar, wind, and geothermal (that we term ‘other renewables’) will overtake nuclear energy in 2024, coal in 2040, oil in 2044, and gas in 2049. Coal production is forecast to decline steadily across the forecast horizon.

In recent years hydrogen has additionally emerged as an potential energy source that could decarbonise sectors such as long-haul transport, chemicals, and steel production, and is included in the ‘other renewable’ energy category. Its future at scale is still uncertain, however given current low levels of adoption in sectors such as transport, buildings and power generation. Currently most hydrogen is produced using fossil fuels but enthusiasm for green hydrogen is growing.

Africa’s energy production profile differs from the global profile, with the more rapid increase in gas production that only peaks at around 2068 before declining. In the Current Path forecast, gas plays a larger role in Africa’s energy future than in comparable regions such as South Asia and South America. Oil production in Africa is also higher than in these regions implying that Africa is particularly dependent upon fossil fuel production, gas and oil in particular, more so than other regions. In the Current Path forecast, coal production in Africa is set to decline as international pressure to reduce fossil fuel production and use mounts and is in line with the various countries’ National Determined Contributions (NDC’s). Gas production in Africa overtakes oil production in 2028, and other renewables are larger than hydro in 2033 and coal in 2042. The result is that Africa’s production of non-fossil fuels as a per cent of the total is significantly lower than the global average.

Much of this is exported from a handful of African countries, meaning that if global coal, oil and gas demand declines, it will affect their exports. Still, it does imply that the continent needs to aim for an early transition from fossil fuels to avoid being trapped with stranded assets.

Alternative energy resources have the potential to play a pivotal role in this transition. Africa has vast capacities for boosting renewables, especially hydropower. Yet, they are currently largely underutilised. In the Current Path forecast, hydro will contribute 5.2% of the continent’s production in 2050, equivalent to less than 0.57 BBOE, with several large hydroelectric schemes currently under construction.

Population growth is an essential reason for the increase in Africa’s future energy demand. In 2023, Africa’s population surpassed that of India and China. By 2063, Africa (at 3.1 billion people) will have almost double the population of India (which will be at almost 1.7 billion). India will, in turn, have a much larger population than China (at 1.2 billion).

Contrary to the situation with these two large countries, Africa’s population numbers will continue to increase beyond the end of the century and as prosperity increases, so will its energy demand and its associated carbon emissions unless the continent embarks upon a different energy future than its current trajectory that imitates the fossil-dependent pathway of richer regions and countries.

The Current Path forecast aligns with the IEA Stated Policies Scenario (STEPS) as presented in their 2023 World Energy Outlook, which would see global demand for coal, oil and natural gas peak before 2030 and their combined share edge downward. Emerging markets, particularly Asia, will take an ever-growing share of demand. Globally, coal is also subject to increased levels of fuel substitution as countries switch to the use of fossil fuels with lower carbon emissions, particularly gas.

The war in Ukraine temporarily created a tight LNG market, resulting in record-high prices in 2022 and a European rush for imports, although 2023 prices were significantly lower. In time, a significant gas supply will come to the market due to the European scramble for alternative supply and the steady increased US production, potentially creating an oversupply towards the end of the decade. Gas is less carbon intensive than coal or oil, but low gas prices may delay the shift to renewables.

There is much attention on renewables, yet the IEA estimates the value of 2022 fossil fuel subsidies at US$1 trillion, which is still much more than renewable energy financing. Thus ‘subsidies for natural gas and electricity consumption [in 2022] more than doubled compared with 2021, while oil subsidies rose by around 85%. The subsidies are mainly concentrated in emerging markets and developing economies, and more than half were in fossil-fuel exporting countries.’

Because China has an outsized role in shaping global energy trends, forecasts for trends for its economy will largely shape future energy demand and carbon emissions. In the last decade, it accounted for almost two-thirds of the rise in global oil use, nearly one-third of the increase in natural gas, and has been the dominant player in coal markets, yet has emerged as a powerhouse in renewables, accounting for around half of wind and solar additions and over half of global electric vehicle (EV) sales. According to the IEA, two-thirds of global wind manufacturing expansions planned for 2025 will occur in China, primarily for its domestic market. Hence, the general view is that China will drive global renewable energy deployment to global benefit.

However, the IEA forecast of China’s growth at just below 4% per annum to 2030 is conservative. Although its growth rate is declining, China may grow more rapidly, emitting substantially more carbon.

While things are also changing rapidly in the US, given its presidential politics, its model is quite different and turbulent. In 2022, fossil fuels accounted for 81% of US primary energy production, nuclear for 8% and renewables including hydro for only 13%. Total energy production in the US has exceeded annual energy consumption since 2019 – a remarkable turnaround for a country previously dependent on oil from the Middle East. Instead of debating energy import dependence, policymakers are seized with decisions for large investments in LNG terminals to export natural gas.

While many high-income countries have enacted policies and laws specific to renewable energy, only half of least developed countries (LDCs) and a third of small island and developing states (SIDS) have done so, finds UNCTAD. Efforts to develop comprehensive legal and regulatory frameworks to advance clean energy technologies are limited mainly to developed and large emerging economies. Instead, countries like Gabon, Tanzania, Liberia, Kenya, Zambia and Angola engage with carbon credit arrangements that do little to reduce emissions. Through a carbon credit scheme, a polluter can buy a carbon credit typically worth one metric ton of carbon dioxide (CO2), with the money paid towards carbon-lowering projects such as protecting natural ecosystems and wildlife resources, planting trees, and generating renewable electricity. Roughly 23% of global emissions are now covered by some form of carbon credit pricing, with the newly established Africa Carbon Markets Initiative (ACMI) aiming to unlock US$6bn in revenue to create 30 million jobs by 2030. These forecasts need to be treated with care, however. The UAE-based Blue Carbon, the company leading most efforts, was, in 2023, barely a year old without any track record in the area (see theme on Climate Futures).

A similar story holds for private investment promotion in renewable energy policies, which is much higher in developed and emerging economies. With limited state resources and amidst competing demands, poor countries struggle to invest in the efforts required to unlock a different pathway to the fossil-fueled example set by others. These findings underpin UNCTAD‘s calls for the international community to help developing countries urgently attract sufficient investment to transition to clean energy. The associated estimation is that developing countries face a US$2.2 trillion annual investment gap for an energy transition to renewables.

Global nuclear power generation is experiencing a renaissance, with significant additional plants being commissioned and planned in the medium to long-term future as countries search for secure energy baseload whilst reducing their carbon emissions. At the 2023 UN COP28 climate summit in Dubai, more than 20 countries agreed to triple global nuclear power capacity by 2050. Initially, much of the growth in nuclear power generation will come from new reactors in China and India and the return of plants in France shut down for maintenance in 2023.

China now accounts for 16% of global nuclear generation, and Russia’s influence in the sector is growing, with the two countries providing the technology for 70% of the reactors under construction.

Energy demand per person: Global comparisons to 2063

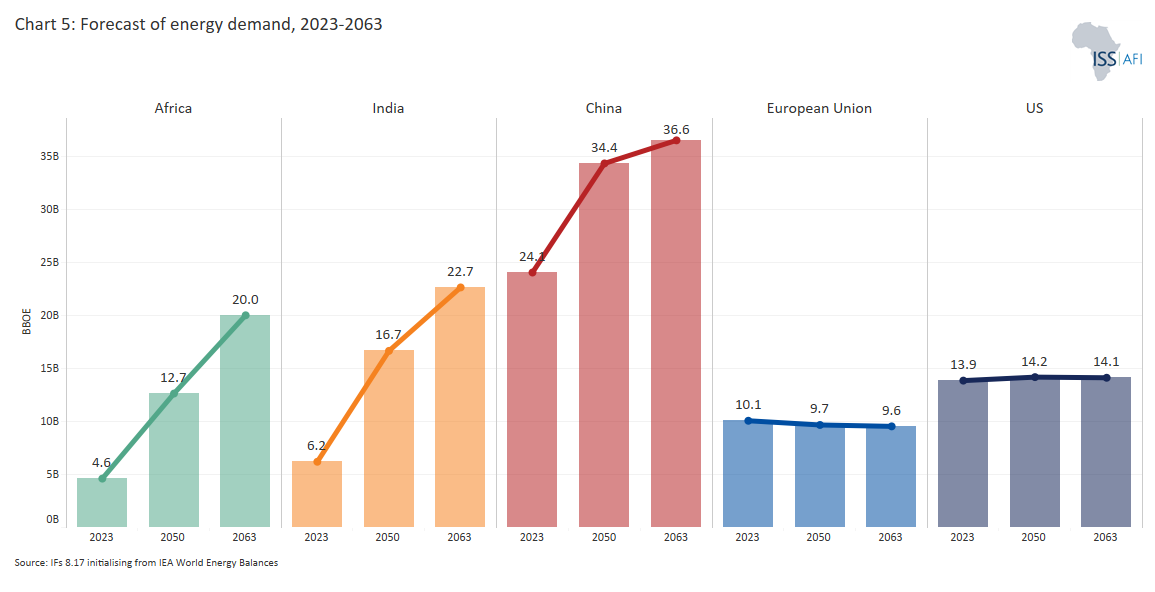

Chart 5 presents the total energy demand at global and regional levels. Annual energy demand (consisting of consumption and unmet demand) in Africa for 2023 differs between countries. It ranges from Libya (18.6 BOE per person) and Mauritius (16.1) to the Central African Republic (0.6) and Burundi (0.5). On the Current Path forecast, Africa’s energy demand will increase to 4.9 barrels per person in 2050 and to 6.4 barrels in 2063, less than a third of the average of the rest of the world. Africa’s energy demand is lower than South America and South Asia, the two other developing regions against which we typically benchmark Africa. The Current Path forecast is that its relative energy poverty (demand per person compared to these two regions) will increase over time as energy production in South America and South Asia ramps up more rapidly than in Africa.

In comparison, the demand from the average American is 40.7 barrels of oil equivalent in 2023, and an Indian 4.3 barrels. By 2050, average US demand will decline to 38.2 barrels, reflecting modest improvements in energy efficiencies. Demand in Africa will then only be slightly higher than India’s currently. By 2063, four decades into the future, Africa’s average energy use per person will be only a fifth of the current demand in the US, 40% of that of South America and 55% of South Asia.

Despite its slow per capita energy demand growth, Africa’s growing population, expanding economy and low energy efficiencies imply that the continent’s portion of the world’s energy demand will increase from 4.9% in 2023 to 13% by 2063. On the Current Path forecast, Africa’s total energy demand will overtake the EU27 in 2043, the USA in 2052, and, by 2065, India. With its much larger population, Africa’s energy demand is already larger than South America’s and should overtake South Asia’s before 2047. By around 2083, Africa’s energy demand will be larger than China’s, pointing to the need to change its current energy mix to unlock a less carbon-intensive future in its own, and global, interest.

Towards a viable Africa Energy Policy

- Briefly

- Reductions in fossil fuel production and use

- Increased non-fossil energy production

- Energy efficiency

- Carbon sequestration

Briefly

Africa needs to transition rapidly to non-fossil fuels, become more energy efficient, and aggressively reduce carbon emissions. We discuss each below and present the results as an Africa Energy Policy scenario reflecting Africa’s energy production and demand on the Current Path forecast. Then, we model a high-growth Sustainable Africa scenario. Forecasts on carbon emissions are discussed in the climate theme.

Reductions in fossil fuel production and use

To meet the challenges of the Paris Agreement to limit global average temperature rise to below 2°C above pre-industrial levels and to pursue ambitious efforts to limit it to 1.5°C, we turn to the UNEP 2023 Production Gap Report[10]: “Phasing down or phasing up?”. The report highlights that under the current government plans and projections, a global ‘Production Gap’ is likely to grow wider out to 2050. This gap shows that governments plan to produce around 110% more fossil fuels in 2030 than would be consistent with limiting global warming to the ambitious 1.5oC target, translating into 69% more fossil fuel emissions that would be considered compatible with limiting global warming to 2oC. UNEP notes that the world only had a 14% chance of limiting warming to 1.5oC. And that fully implementing efforts implied by unconditional national commitments would put the world on track to 2.9oC. There is a large gap, the authors warn, between the fossil fuel production that is being planned and pursued and the Paris Agreement’s global warming limits pointing to the need of drastic change.

To keep the 1.5oC ambition alive, fossil fuel use must decline dramatically and other key mitigation and sequestration efforts must increase exponentially. The Production Gap report recommends that the world aim for a near-total phase-out of coal production and use by 2040 and reduce oil by three-quarters by 2050 compared to 2020 volumes. Africa will undoubtedly require significantly more energy in the future, but two caveats are important in considering the contributions from fossil fuels.

The first is that government revenues from fossil fuel production projects are often grossly overestimated in the pre-production process. The reasons vary and include the complex tax avoidance schemes that typically accompany such large-scale private investors (through, for example, the establishment of special purpose vehicles in tax havens such as Dubai) to avoid withholding taxes on dividends and interest. Thus a recent study of 12 African countries which exploited oil and gas resources between 2001 and 2020 found that revenue forecasts were exaggerated by an average of 63%.[11] Our work on the future of Mozambique which has some of the largest gas reserves in Africa, confirms the extent to which the subsequent government revenue streams will only realise several decades in the future and then at modest levels with little trickle-down effects – unless the government of Mozambique implements appropriate policies to avoid the Dutch disease effect and to ensure inclusive development benefits..

The second caveat is the damage associated with the Dutch disease (over-reliance on a single commodity for export revenues). The negative effect is well documented and briefly discussed in the Current Path theme. Instead of economic diversification, more African countries are becoming single-commodity dependent and hence trapped in a low-growth future, vulnerable to swings in commodity prices and global disruptions.

However, in considering these caveats, it is also important to recognize the opportunity that fossil fuel exploration projects offer to a continent that otherwise attracts limited foreign direct investment. Although trends are changing, the resource extraction sector (mining, oil and gas), attracts the bulk of Africa’s FDI, implying that pressure to avoid these sectors amongst foreign investors could have a significant detrimental impact on a continent in dire need of capital.

The realisation of the Production Gap goals set out by UNEP is ambitious. According to the Current Path forecast, coal will still account for 18% of global energy production in 2040 (equivalent to 21.3 BBOE). By 2050, oil would account for 22% (equivalent to 30.2 BBOE) and gas for 29% (equivalent to 38.6 BBOE) of production. Therefore, the transition proposed by the Production Gap Report requires that 63% of global energy production in 2050 shift from coal, oil and gas to other energy sources, equivalent to 87 BBOE.

To explore the impact of the UNEP production gap targets on Africa, we undertook a separate sensitivity study to examine the impact of these reductions on the affected African fossil fuel producers.

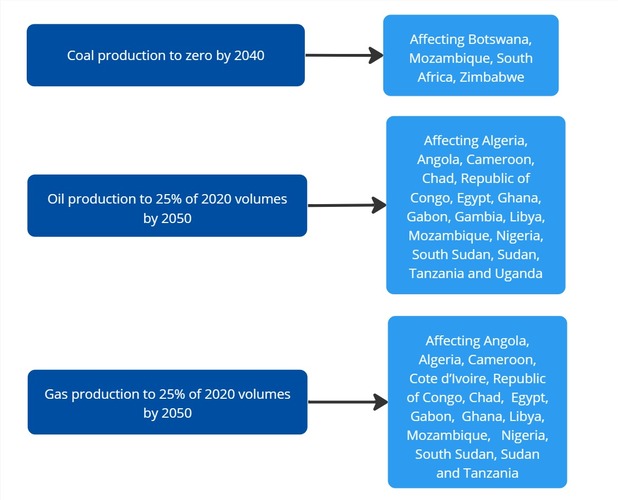

Chart 7: African countries affected by the UNEP Global Production Gap recommendations

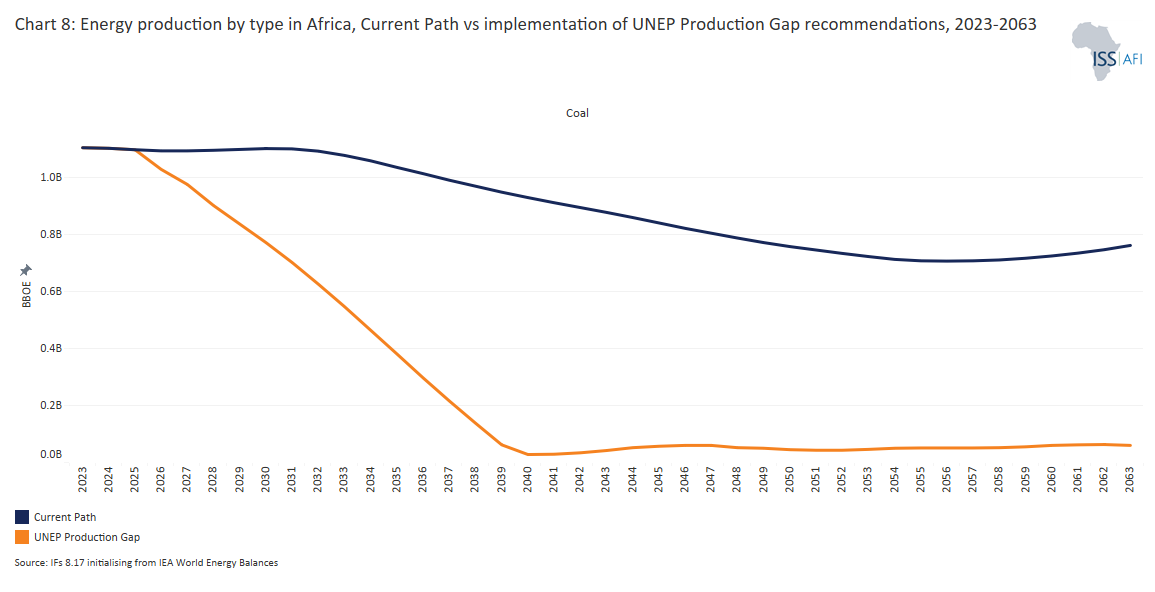

The results are reflected in Chart 8, which compares energy production by type in the Current Path forecast with the UNEP Production Gap recommendations.[12]

Africa’s total energy production in 2023 was equivalent to 6.3 BBOE. Implementing the UNEP recommendations implies that Africa’s total energy production, much of which is currently exported, will decline to 4.9 BBOE (instead of 10.9 BBOE) in 2050. The continent would produce 6 BBOE less energy than in the Current Path forecast.

Implementing the UNEP recommendations will require African countries to pay US$231.3 billion more for energy imports in 2050 while Africa’s energy export earnings will decline by US$214.4 billion – a total difference of US$446 billion. The effects will be disproportionate on the twenty or so fossil fuel producers. Some of the effects include a deterioration in the current account balances and increased debt, but, in time, the result is a more productive and diversified economic structure that is not affected by the ills associated with single commodity dependence. After an initial painful adjustment period (lower energy exports, higher energy imports), total African export value in 2050 will be slightly higher and imports slightly lower (by about 2% in both instances).

Increased non-fossil energy production

Africa must increase non-fossil energy production to compensate for reduced fossil fuel production.

According to a 2023 report from the IEA, a tripling of energy production from renewables by 2030 is “technically and economically feasible”, but requires significant policy and investment changes.[13] These ambitions were affirmed at COP28 later that year which agreed to target to triple renewable energy capacity to at least 11 000 GW by 2030, is now within reach with more rapid progress in China. African governments have already more than tripled public investment in renewable electricity, up to US$47.0 billion from US$13.4 billion the previous decade. Many African countries have also set ambitious targets for renewable energy development, typically 30% in 2030, although often from a shallow base. Some, such as Kenya and Cape Verde, aspire to 100%. Others, such as Mozambique, Rwanda and Eswatini, aspire to around 60%.

The reasoning for more rapid decreases in the costs of other renewables follows findings from the International Renewable Energy Agency (IRENA) that renewable energy costs have steadily fallen for years. Between 2021 and 2022, for example, the global weighted average cost of electricity from new onshore wind projects dropped by 5% and solar PV by 3%. These trends will likely continue, driven by technological advancements, economies of scale and competitive market dynamics. IRENA projects that by 2050, the cost of electricity from utility-scale solar PV could fall by as much as 80% compared to 2020 levels, while onshore wind could see a cost decline of 50%.

The IEA Africa Energy Outlook 2022 report projects that under ambitious policy interventions and significant investments, Africa could see over 80% of new power generation capacity coming from renewables by 2030.

In their World Renewables Outlook 2023report, IRENA estimates that Africa could achieve a renewable energy capacity of 750 GW by 2030, representing a four-fold increase from the current capacity of roughly 180 GW. However, the increase comes from a shallow base.

In 2023, the contribution from renewables only constituted 106 MBOE (or 1.7% of total energy production) and was set to increase to 266 MBOE in 2030, i.e. by a factor of 2.5.

Nuclear will likely also play an important role in Africa’s energy future. For the first time since the annual climate summits commenced in 1995, the 198 signatory countries to the UN Framework Convention on Climate Change (UNFCCC) officially included nuclear energy to help achieve deep and rapid decarbonisation at the COP28 meeting in Dubai in December 2023. The inclusion of nuclear and a separate declaration by more than 22 countries to advance the aspirational goal of tripling nuclear power capacity by 2050, on top of statements by the IAEA and the nuclear industry, underscored a new momentum for this sector and its potential contribution to clean energy.

The enthusiasm for nuclear energy follows future technological developments nearing production-level maturity. Micor, small and medium-scale modular reactors (MMRs, and SMRs)[14] that are factory-built and standardised could eventually benefit from economies of scale, with simplified design, fuel efficiency, reduced nuclear waste management costs and hence faster deployments and lower construction costs with the potential to be ratcheted up or down to help balance the grid alongside surging renewable output in a decade or so. Larger units providing 1 GW or more would provide substantial additional base-load capacity.

Some studies suggest SMRs could achieve a levelized cost of electricity competitive with renewables by 2030-2040, while others estimate higher costs and slower cost reductions. It is unclear if these comparisons factor in the simultaneous expected reductions in renewable costs to allow for a like-to-like comparison. The IEA estimates current overnight capital costs for SMRs to be 4-7 times higher than large-scale reactors but expects significant reductions with further development and deployment.

In addition to nuclear, Africa also has to invest in more energy from hydropower – although the associated projects are often capital intensive and require significant lead-in times. In a meeting of the International Hydropower Association in Abuja during May 2024, participants called for refurbishment of Africa’s aging hydro facilities and for African governments to ‘recognise and champion sustainable hydropower as a clean, green, modern and affordable solution to provision of secure electricity supply…’

A recent additional concern is the extent to which the increased variations in seasonal rainfall that are associated with climate change are making hydropower less reliable with each passing year. Thus, in February 2024, Zambiaextended its national disaster to include a provision to import and ration electricity as a devastating drought affected hydropower generation from the Kariba Dam, its main source of energy. The effect is being felt globally. According to the IEA, droughts were an important contributing factor to higher world energy demand in 2023, worsened by the El Nino weather pattern that warms the Pacific Ocean. To compensate, fossil fuel power plants were used instead, releasing about 170 million tons of additional CO2.

These considerations point to a degree of caution in the extent to which hydropower could be extended.

At this point it is important to pause, for our analysis indicates that it will not be possible to close the 5.9 BBOE production gap[15] that will be left with the ending of coal production by 2040 and a drastic reduction in oil and gas by 2050 as recommended by UNEP. Even the most optimistic increases in hydro, other renewables and nuclear production will be insufficient. Nor is it likely that Africa will be able to source sufficient energy through imports (even if it can fund the US$445.7 billion gap mentioned above) since the pursuit of the UNEP targets globally will constrain available fossil energy sources for import from other regions in the world.

After consideration of the impact, we, therefore, remove the constraints on gas production but maintain the UNEP targets for reductions in coal and oil in the subsequent scenarios.

Energy efficiency

In addition to the use of different sources of energy, fossil fuel dependence can also be reduced by improving the efficiency with which the fuel is used. Africa requires 70% more energy per unit of GDP than the global average, reflecting the potential for rapid improvement.

There are numerous commitments and plans to improve energy efficiencies, particularly championed by IRENA which argues for an aggressive energy efficiency strategy as a critical component towards emission reduction. At COP28, countries agreed to double the average annual rate of energy efficiency improvements to four per cent by 2030 and reduce methane emissions.

In the Africa Energy Outlook 2022, the IEAprojects that with vital policy interventions and significant investments, Africa could achieve a 30% reduction in electricity demand through energy and material efficiency measures by 2030. However, in 2023, the electricity share of energy use in Africa averaged only 13% and is forecast to decline to 11% in 2050, meaning the reductions in electricity demand would have a negligible impact on total energy demand, particularly given energy poverty. Additional savings could come from implementing stricter building codes and energy standards, greater industrial efficiencies such as in cement, steel and chemicals (the ADB estimates this could save up to 10% of the continent’s total energy consumption by 2030), and efficiencies in existing vehicles and promoting fuel-efficient modes of transport, which the IEA estimates could contribute a 5-10% reduction in total energy demand by 2030.

Africa has small, fragmented and inefficient electricity grids, as reflected in a recent innovative display developed by the World Bank. Among many other measures, improvements in connections within and between countries and Africa’s five power pools (or regional networks) will significantly improve electricity access and reduce inefficiencies. An essential step in this regard occurred in June 2021 when the African Union launched the Africa Single Electricity Market (AfSEM) to be supported by the Continental Power System Masterplan currently being developed by the African Union Development Agency (AUDA-NEPAD).

Because it relies upon fossil fuels (mostly diesel) that are transported by road (and not by rail or pipeline), often for use in numerous small generators, the potential for greater energy efficiencies in Africa with fossil fuel use is significant.

Carbon sequestration

The theme on climate details Africa and global carbon emissions and the goals to limit global warming. It analyses associated trends on changes on the continent and their attendant effects. Carbon sequestration and storage are integral to efforts to combat climate change.

Africa was responsible for a mere 4.6% of global carbon emissions from fossil fuels in 2023, increasing to 11.3% in 2050 and 18% in 2063. However, it has significant carbon sequestration potential[16] due to its vast forests, savannah and grassland areas. According to the FAO, 21% or about 632 million hectares of Africa is forested, while land classified as grazing accounts for 29% (881 million hectares), significantly larger than cropland, constituting a mere 10% (296 million hectares). According to the 2019 IPCC Special Report on Climate Change and Land Summary for Policymakers: ‘All assessed modelled pathways that limit warming to 1.5ºC or well below 2°C require land-based mitigation and land-use change, with most including different combinations of reforestation, afforestation, reduced deforestation, and bioenergy.’

Energy Scenarios

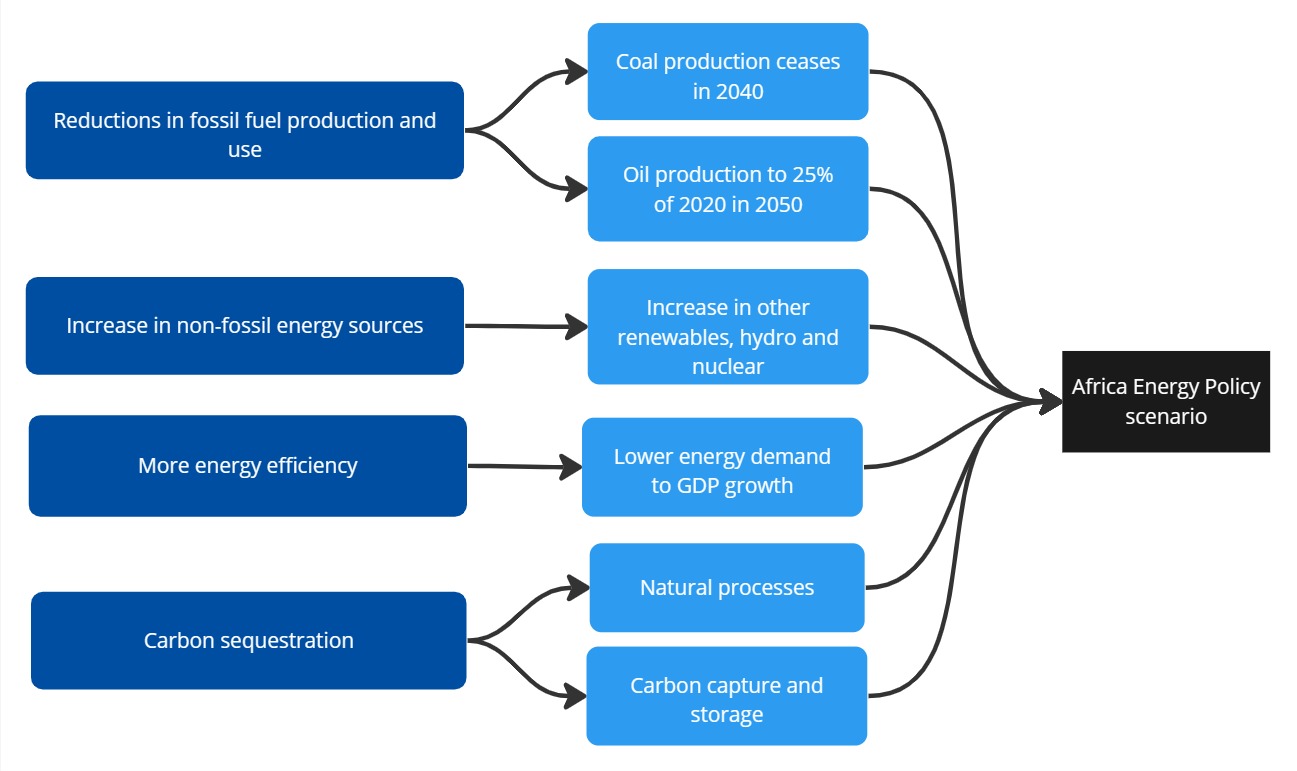

Based on the benchmarking and analysis done in the previous sections, it is now possible to present an Africa Energy Policy scenario. Our modelling consists of four intervention clusters:

- Government policies and actions that end coal production by 2040 and reduce oil production by 2050;

- Ambitious increases in Africa’s energy production from other renewables, nuclear and hydro;

- Institutional, management, technological and infrastructure improvements leading to more energy efficiency, thus reducing energy intensity (demand to GDP); and

- Carbon sequestration to reduce the carbon generated by burning coal, oil and gas[17] including forest regeneration[18], carbon capture and storage and improved land management.

Our scenario does not include a carbon tax. Some countries are phasing in such taxes, but it is unlikely that Africa would lead on such policies; instead, it would join a global effort in this regard and even then belatedly. We explore the impact of a global carbon tax in the climate theme in four alternative scenarios, ranging from a universal tax (Everyone Pays scenario) to a tax on high emitters only (Polluters Pay scenario).

Chart 9: Africa Energy Policy scenario

The Africa Energy Policy scenario reflects Africa’s energy demand and production on its likely future development pathway. It would see average economic growth amongst African economies of 4.7% from 2024 to 2050.

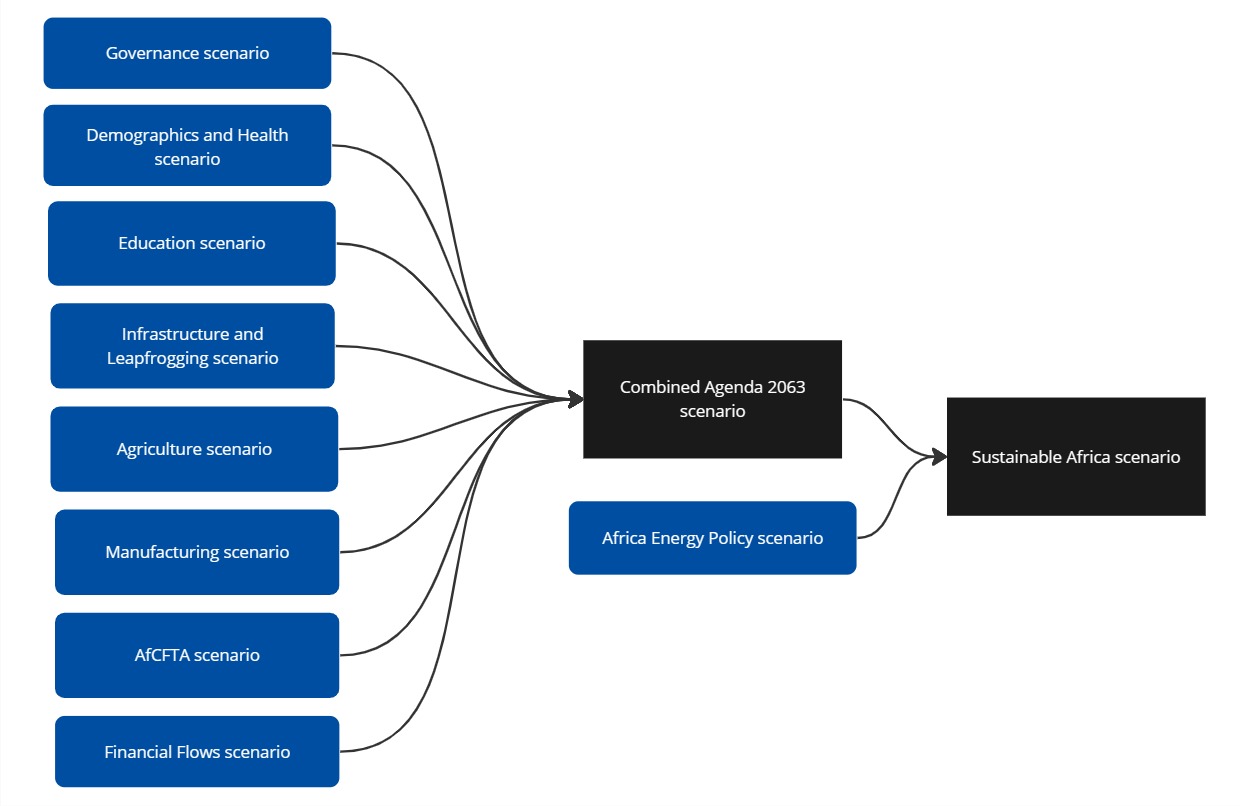

In the final step (Chart 10), we develop our Sustainable Africa scenario. It combines the Africa Energy Policy scenario with the Combined Agenda 2063 scenario, which consists of eight sectoral scenarios that advance Africa’s development prospects (ranging from agriculture to manufacturing and the full implementation of the AfCFTA). Chart 10 presents the composition of the Sustainable Africa scenario. In this scenario the average economic growth rate if 7.7%.

Chart 10: Sustainable Africa scenario

Comparing Energy Scenarios

In this section, we compare Africa’s Current Path or likely development trajectory with the impact of the two scenarios presented in the previous section:

- The first is the Africa Energy Policy scenario that dramatically reduces fossil fuel use, increases non-fossil fuel production and applies various mitigation policies; and

- The second is the Sustainable Africa scenario, which applies the Africa Energy Policy scenario to a high-growth future.

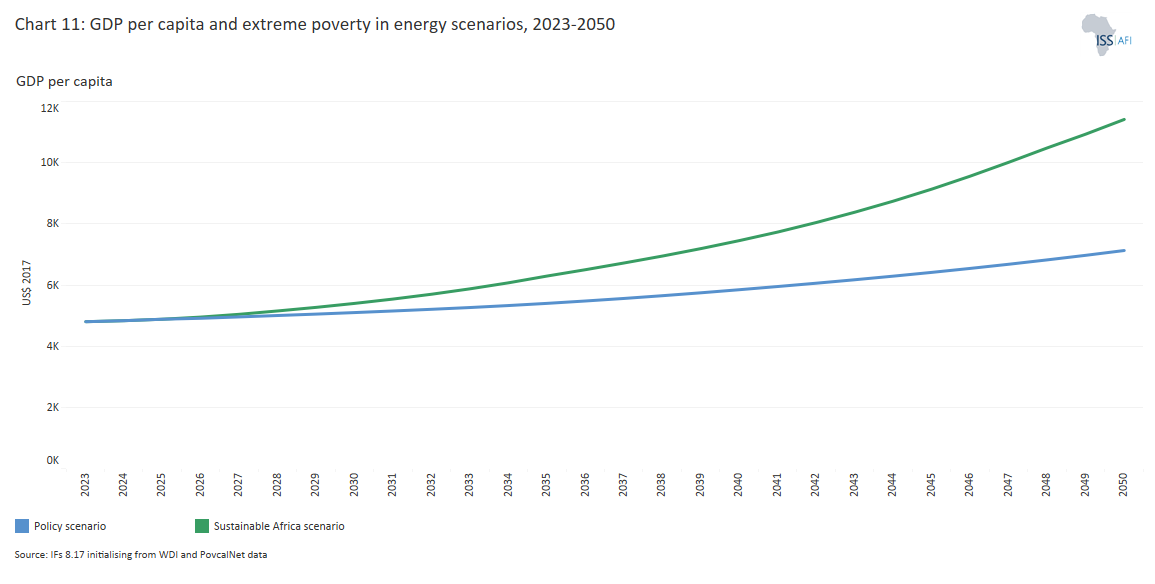

As a first step, Chart 11 presents GDP per capita (or extreme poverty – the user can choose) in the Current Path/Africa Energy Policy scenario compared to the Sustainable Africa scenario. It serves to illustrate the large difference in development outcomes between these two scenarios and serves to remind the reader that it is only the energy mix that changes in the Africa Energy Policy scenario. Africa’s development outcomes are unchanged from the rather uninspiring Current Path forecast.

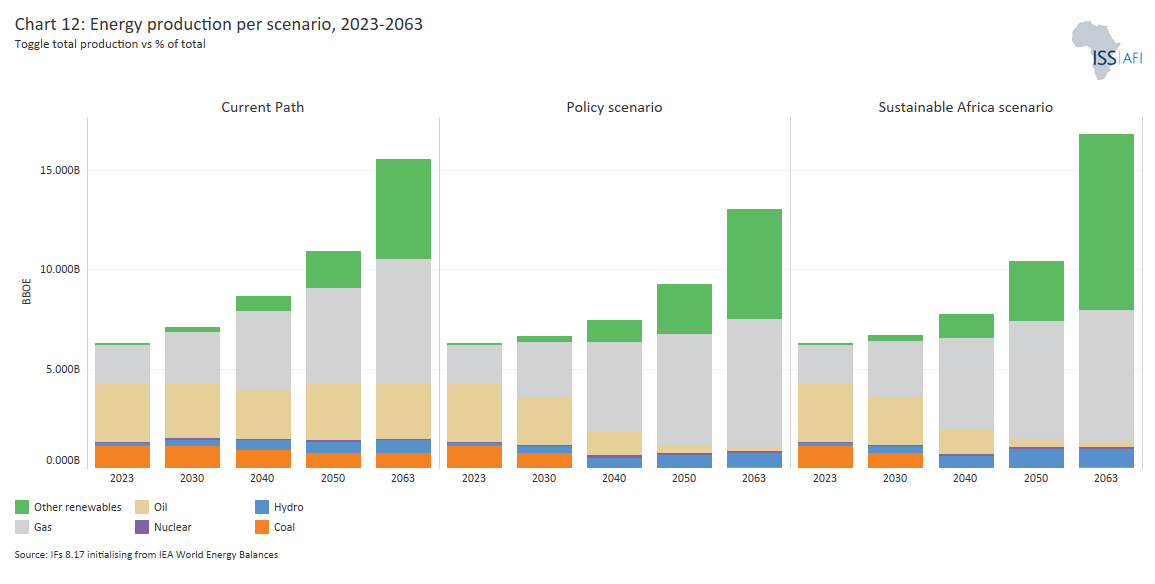

Chart 12 allows the user to view energy production per type of energy for each African country and region. The user can choose between the Current Path, the African Energy Policy scenario (with its changed energy mix) and the Sustainable Africa scenario (that represents the energy mix in a high growth future consisting of the African Energy Policy scenario and the Combined Agenda 2063 scenario). In summary

- The Africa Energy Policy and Sustainable Africa scenarios see an end to coal production by 2040 while oil production declines to below 400 MBOE by 2050. The 2050 Current Path forecast is 2.8 BBOE.

- The 2050 Current Path forecast for Africa’s gas production is 4.8 BBOE. It increases to 5.6 BBOE and 5.9 in the Africa Energy Policy and the Sustainable Africa scenarios, respectively.

- An increase in energy production from other renewables (excluding hydro) by 33% above the Current Path forecast in 2050 and 150% in the Sustainable Africa scenario.

- An increase in energy production from hydro by 13% above the 2050 Current Path forecast.

- Greater energy efficiency that reduces Africa’s energy demand (i.e. the amount of energy required to increase the size of the economy by a set amount) by 4.2% below the 2050 Current Path forecast.[18]

- An increase in nuclear energy production of 52% and 68% for the two scenarios above the 2050 Current Path forecast. The increase in Africa’s nuclear energy production is small in absolute terms. Should the promise of SMRs come to fruition, nuclear has potential to make a large constribution to meeting Africa’s base-load energy demand.

The Africa Energy Policy scenario reflects Africa’s energy demand and production on its likely future development pathway. It would see average economic growth amongst African economies of 4.7% from 2024 to 2050. By 2050, we anticipate that Africa’s energy production would be 1.7 BBOE below the Current Path forecast, and 2.5 BBOE by 2063. A reminder that in this scenario Africa ends coal production by 2040, reduces oil production significantly but increases gas production by 17% in 2050, tapering off thereafter. The gas production increase is at 23% (2050) in the Sustainable Africa scenario. The increase in gas production in the Africa Energy Policy and Sustainable Africa scenarios is, however, insufficient to compensate for the reductions in energy from coal and oil. As a result:

- In the Africa Energy Policy scenario energy imports increase by US$108 billion (2050) and US$326 billion (2063), reflecting a growing energy production gap.

- The gap increases further with the Sustainable Africa scenario. In that scenario Africa imports US$397 billion more energy in 2050 and US$1.3 trillion in 2063.

In the Current Path forecast Africa becomes a net energy importer in 2041, paying more for energy imports than it gains from exports. In the African Energy Policy scenario, it happened five years earlier, and eight years earlier in the Sustainable Africa scenario, with obviously large national variations.

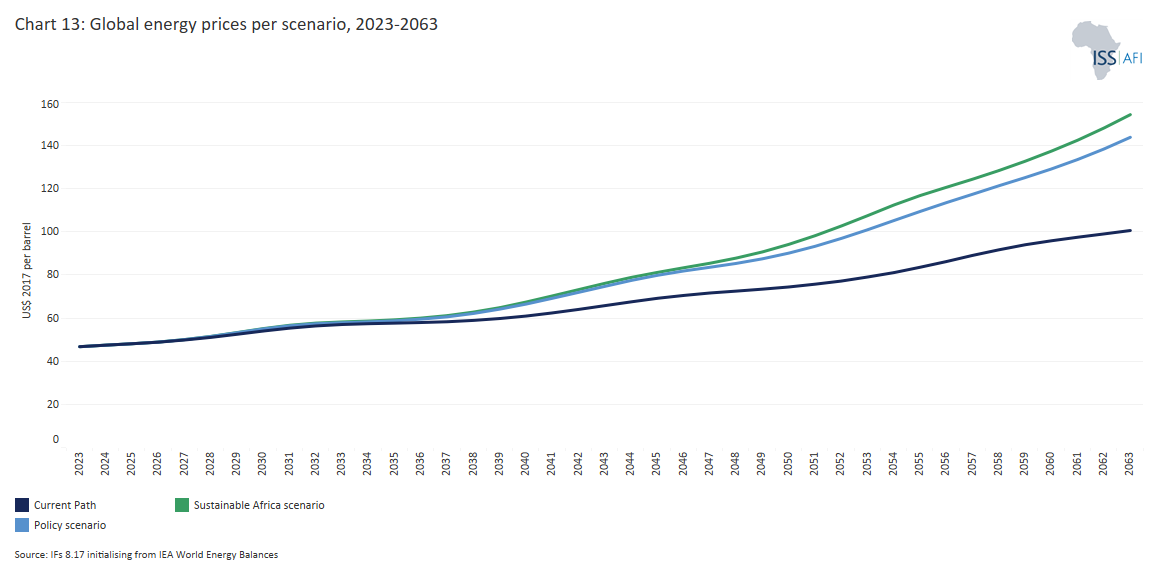

Chart 13 reflects the rapid change in Africa’s energy production landscape over time comparing scenarios, particularly among Africa’s 20 coal, oil and gas producers. Countries that do not produce coal, oil or gas, will be less affected and their transition to a sustainable growth path is much easier.

Although Africa is a small energy producer, the scenarios will affect world energy prices. Average global energy prices change with each scenario and the associated forecast is provided in Chart 13.

By 2050, much will have changed compared to 2023. The world population will have increased by 1.7 billion additional people to 9.7 billion, the world economy will be US$97 trillion[19] larger and GDP per capita will have increased by 49%[20].

Africa and its relationship with the rest of the world will also change. Instead of constituting 18% of the world’s population, by 2050, Africans would represent 26.5%. Africa’s portion of GDP, 2.9% of the world in 2023, will be 4.8% in 2050 and, in the Sustainable Africa scenario, Africa would constitute 8.3% of the global economy.

The progress is reflected in the degree to which Africa will achieve almost total electricity access by 2050, although a handful of countries, Burundi, South Sudan, Central African Republic and Chad still have less than 60% access, but making rapid progress.

The fulfilment of the Sustainable Africa ambition would see a 2050 African economy that is 79% larger than the Current Path forecast. GDP per capita would be 61% higher and only 105 instead of 356 million Africans would be living in extreme poverty. African countries would, on average, grow roughly two percentage points more rapidly than in the Current Path forecast for 2050.

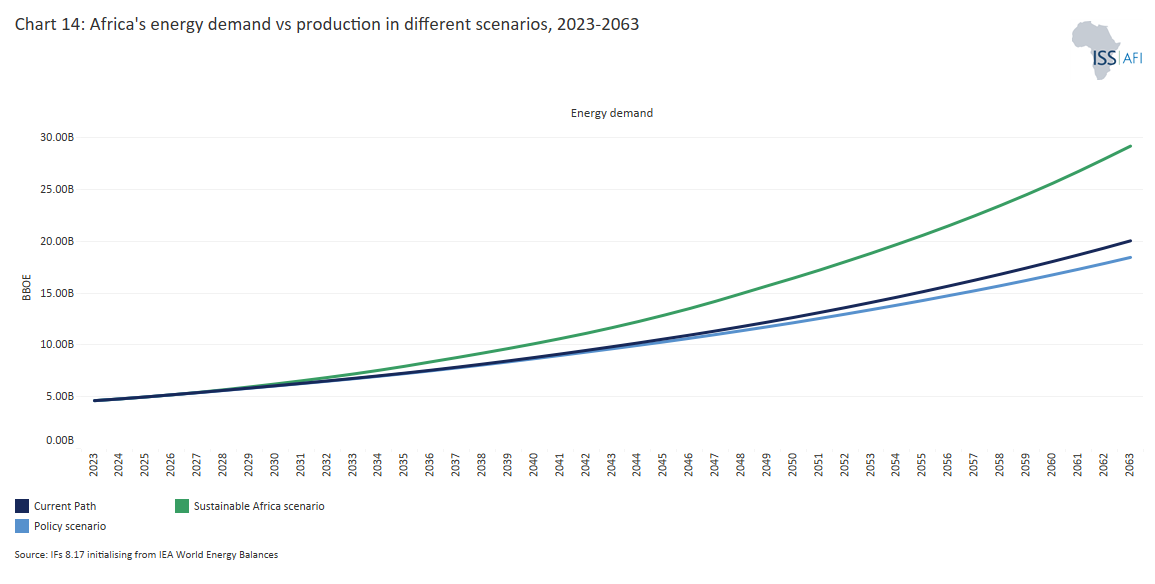

Chart 14 compares Africa’s total energy demand with production and allows the user to select the data for any African group or country from the drop-down menu to compare the three scenarios. Energy demand in the Sustainable Africa scenario is significantly larger than in any other scenario, given the associated push on all aspects of growth including manufacturing and trade.

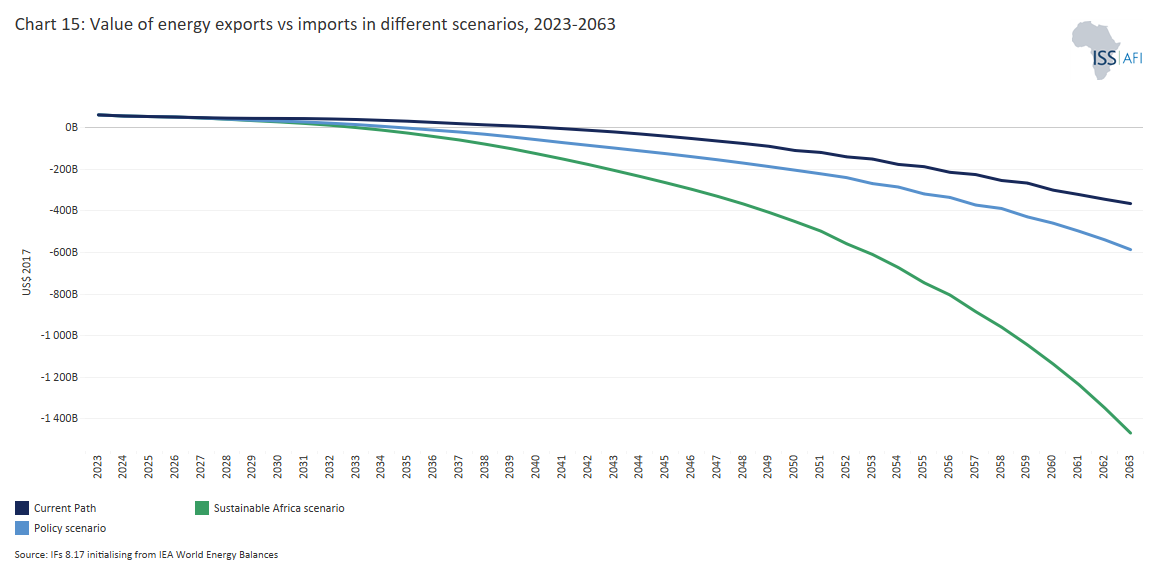

The gap between the 2050 demand and production forecast on the Current Path would be 1.76 BBOE scenario, 2.9 BBOE in the Africa Energy Policy scenario and 6 BBOE in the Sustainable Africa scenario. A previous section presented the extent to which Africa is currently a net energy exporter despite its domestic energy poverty. Over time that surplus will decline implying that many more African countries would have to import more energy. Chart 14 compares the value of future exports with imports. It reflects that Africa will become a net energy importer in all scenarios and the extent to which its energy import dependence increases most markedly in the Sustainable Africa scenario. The effect will fall disproportionally on the continent’s current oil and gas exporters.

A previous section commented on Africa’s low levels of energy demand per capita (at 3.2 barrels of oil equivalent per person in 2023 compared to an average for the rest of the world of 13.6 barrels) – see Chart 6. African energy demand is significantly below comparable regions such as South America and South Asia. The analysis referred to the importance of sufficient energy for development, noting a consensus pointing to a minimum requirement of 8.6 barrels per person per annum and reflected on the fact that Africa, on average, does not achieve this minimum requirement, even by 2063 with an average demand on the continent at 6.4 barrels per person then. However, in the Sustainable Africa scenario the average continental demand crosses this threshold in 2056 and increases to 10.7 barrels by 2063.

The impact of the suite of policies to improve energy efficiency and constrain carbon emissions is evident when considering that Africa will, in 2050, release 4.3% less carbon from fossil fuels in the Sustainable Africa scenario compared to the Current Path forecast. However, more rapid economic growth in the Sustainable Africa scenario eventually translates into more emissions. By 2063 Africa will release 6% more carbon from fossil fuels in the Sustainable Africa scenario than in the Current Path. So, with the implementation of an aggressive suite of mitigation measures, Africa could grow at an average of 7% per annum (instead of 4.7% on the Current Path forecast) while its carbon emissions only increase above the Current Path forecast three decades into the future.

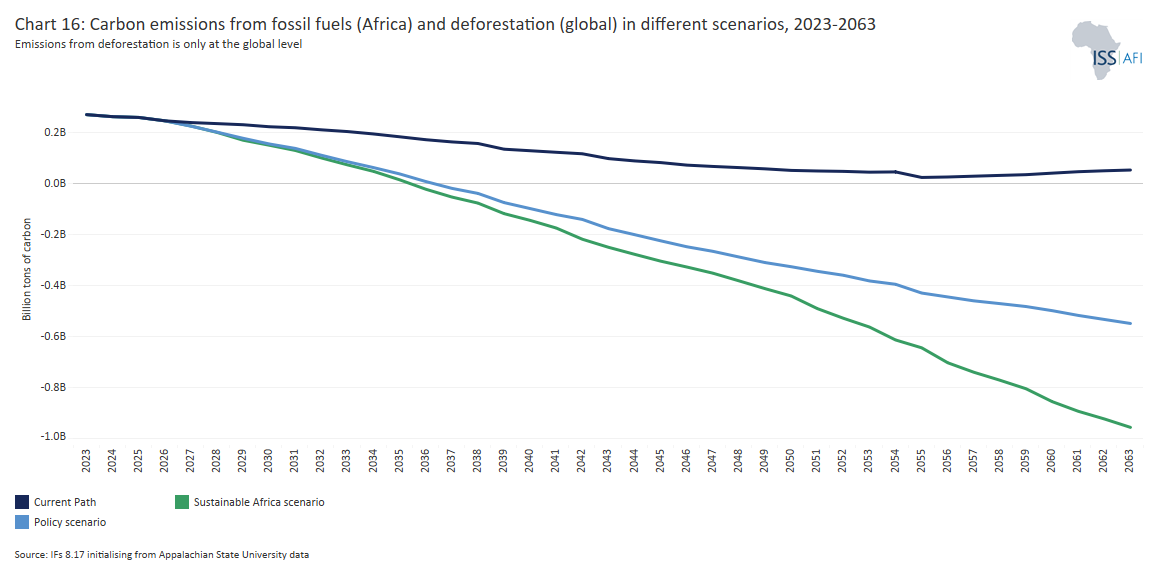

The reason for the lower than expected carbon emissions in the Sustainable Africa scenario comes from the decline in deforestation and, eventually, from around 2040, reforestation that we use as a proxy for a range of policies, including restoring grasslands and better land management.[21] The result is that instead of 576 million hectares of forest in 2050, Africa will have 622 million hectares – an 8% difference. This large difference would require an ambitious departure from current slash-and-burn farming practices and a dedicated effort towards reforestation and improvements in general land management. In the Sustainable Africa scenario, forests absorb an additional 493 million tons of carbon (or 1.8 billion tons of CO2 equivalent). See the theme on Climatefor more details.

Rather than its ability to constrain all fossil fuel production, Africa’s most significant contribution to a sustainable future is the extent to which it has the potential to act as a carbon sink through the application of policies on reforestation, improved land management and associated measures. This could serve as an essential incentive for investment and the purchase of carbon credits. In the Current Path forecast global carbon emissions from deforestation will decline from 200 million tons in 2023 to 36 million tons in 2050. In the Africa Energy Policy scenario, global reforestation increases carbon absorption to 347 million tons, and to 457 million in the Sustainable Africa scenario (see Chart 16).

The impact of the mitigation and adaptation measures modelled as part of the Sustainable Africa scenario is powerful. Although it will not be easy, Africa can embark upon a sustainable growth path to its own and global benefit – but only if it has the room to exploit its gas resources to avoid an energy and financial crisis, reflecting a more modestly scaling back on fossil fuel use compared to the UNEP recommendations.

There are many ways in which Africa can progress towards more sustainable energy use in addition to those modelled in this theme. In addition to determined efforts to increase renewable energy production, build hydroelectric schemes, and extend nuclear while simultaneously removing coal production and dramatically reducing oil production, on top of the various mitigation efforts, Africans and the international community would need to think creatively about the future including giving serious attention to the repurposing of solid waste as one obvious avenue to pursue. See the theme on climate for more details.

Conclusion: Challenges of achieving a Sustainable Africa Energy Future

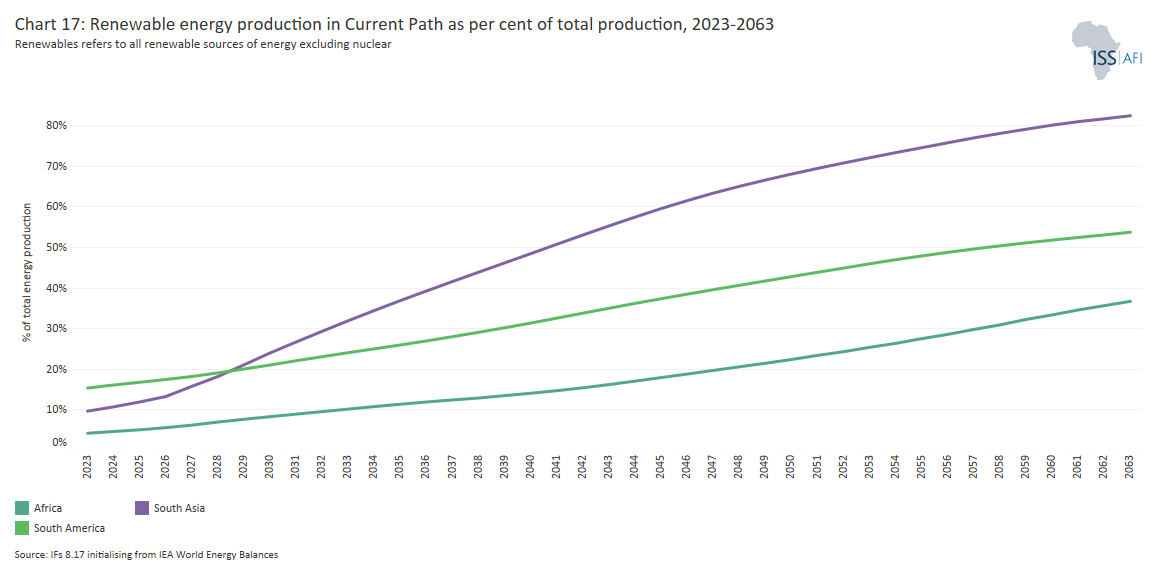

In 2023 Africa only produces 1.5% of its energy from renewables (excluding hydro). The other two developing regions, South Asia and South America produced 3.6% and 5.6% respectively. By 2050 Africa will produce around 16% while the other two regions will produce almost half of their energy from renewables. Africa will trail further and further behind. Expressed as a portion of total energy production, South Asia and South America also produce more nuclear and hydro than Africa. There are significant variations between sub-regions and countries, of course. North Africa is much more dependent on fossil fuels compared to Sub-Saharan Africa. However, because the latter has a poorly developed energy infrastructure, it is less tied to the path dependency of other regions. The result is that Sub-Saharan Africa is well positioned for an energy transition in line with the policies advocated in the UNEP Global Gap report, with the potential to transition to non-fossil energy sources rapidly. North Africa is less so. Should the promise of SMRs come to fruition nuclear is all poised to play an important role in meeting Africa’s base load requirement as well as contributing to a lower-carbon trajectory.

Our modelling suggests a first estimate of a carbon budget for Africa in the order of 13% of total emissions from fossil fuels by 2050 and 22% by 2063. That would be the share of global emissions from fossil fuels that Africa would require in the Sustainable Africa scenario, i.e. in an ambitious high-growth scenario that includes a host of mitigation policies and efforts to constrain carbon emissions whilst rapidly transitioning away from coal and oil.

In considering these numbers, the reader is reminded that Africa’s 2050 population will constitute 25% of the world’s total and, in 2063, it will be 28%. Currently Africa constitutes 18% of the world’s population. Therefore, Africa’s required share of carbon emissions from fossil fuels is significantly below its share of the global population, even on a high-growth forecast. Currently, Africa contributes 4.8% of global carbon emissions from fossil fuels. The Current Path forecast, i.e. on Africa’s current modest development trajectory, is 11% and 17%, respectively. Bear in mind that the African population is smaller in the Sustainable Africa scenario, given the reductions in fertility rates that accompany improvements in well-being. The difference in emissions from fossil fuels between the Current Path forecast and the Sustainable Africa scenario is 46 million tons of carbon (169 million tons of CO2 equivalent) in 2050 and 85 million tons (312 million tons of CO2equivalent) in 2063.

In 2023, Sub-Saharan Africa produced 5.5% of its energy from wind, solar and geothermals (6.1% if hydro and nuclear are included), and North Africa produced only 2% with the inclusion of hydro and nuclear. The Current Path forecast is for a rapid increase in renewables to the extent that, by 2050, Sub-Saharan Africa will generate 27.4% of its energy from renewables and 52.5% in the Sustainable Africa scenario. These significant increases reflect the potential for rapid progress in the region, with slower improvements likely in North Africa.

The role that hydrogen could play in Africa’s energy future is currently unclear. Energy from hydrogen has regularly attracted hype and disillusionment, and its journey towards becoming a ubiquitous fuel is bumpy at best, given the challenges of producing, transporting and containing it. The most straightforward use of large-scale hydrogen is in hard-to-decarbonise areas of the economy, such as heavy industry, with limited application in Africa, given the low demand from these sectors. It is, instead, the potential for export that attracts attention. Thus, with promises of US$10.8 billion investments from Germany, Namibia has the most ambitious plans to produce green hydrogen from its abundant solar and wind resources, turn it into ammonia, and then ship it to Europe.

With clear policies and determined leadership, many African countries can embark on an early transition to reduce fossil fuel use, as presented on this page. Large fossil fuel producers, Nigeria, South Africa, Algeria, Egypt, Angola and Libya will be most affected. The future carbon emissions from a handful of African countries are globally significant, namely Nigeria, Egypt, South Africa, Ethiopia, Algeria, the DR Congo, Mozambique, Tanzania, Uganda, Côte d’Ivoire, Morocco, Sudan and Zimbabwe. These are countries with rapidly growing populations and fossil fuel importers or producers. Their success in transitioning quickly to renewables and reducing their carbon footprint will be critical in determining Africa’s contribution to global warming and a sustainable global future.

Amongst Africa’s coal producers, South Africafaces the most significant challenge in meeting the Global Gap report target of eliminating coal production by 2040. In 2023, it depended on coal for almost 95% of total energy production and is one of the largest coal exporters in the world. As a result, South Africa is Africa’s largest carbon emitter, the 15th largest carbon emitter of fossil fuels globally and includes some of the most air-polluted areas in the world. According to the Current Path forecast, South Africa will still depend on coal for 74.4% of its total energy production in 2040 while also exporting large amounts. In the Sustainable Africa scenario, South African energy exports will decline to about US$2.7 billion in 2050 (compared to the Current Path forecast of US$12.7 billion), and energy imports will increase by US$29.4 billion. The associated energy transition would be huge but outweighed by the benefits to its economy and the health of its citizens.

Similar to other large coal exporters, the South African government and proponents of a rapid transition away from coal have to contend with a strong coal lobby, including from unions in its mining sector. In the interests of reductions in carbon emissions and in addition to a substantive investment in CCS, there is no alternative to a rapid decrease in coal production and consumption globally.

The transition from coal will also be painful for Zimbabwe, Mozambique and Botswana. The latter sourced 50% of its energy production from coal in 2023 – Zimbabwe was 71% and Mozambique at 57%. On the Current Path forecast, coal production in Botswana will remain at its current levels until 2050, while production in Mozambique and Zimbabwe is set to increase, implying that these countries could continue mining coal for domestic energy production given the size of known coal reserves, but that they will have to forego export earnings related to their coal assets since they would struggle to find external investors and markets.

Africa’s oil exporters, such as Angola and Libya, will also need help reducing production in line with the UNEP target. Nigeria, Africa’s largest oil producer, will be challenged the most. Oil accounts for over 80% of exports and roughly 50% of the government budget, although production has steadily declined from its peak in 2005. Investments in exploration have also gone down. Many of the larger foreign oil companies such as Shell, TotalEnergies, Chevron, ExxonMobil, Eni and Equinor have either left, are in the process of doing so, or are shifting their investments into offshore waters given high levels of insecurity onshore, particularly in the Niger Delta that harbours most of Nigeria’s onshore and shallow-water oil rigs. With the largest gas reserves in Africa, Nigeria will inevitably pivot from oil to natural gas, which currently accounts for just 10% of Nigeria’s exports. Increasing its gas exports would require significantly expanding the facilities to cool and liquefy gas, writes the Economist.

On the one hand, our modelling indicates a slow energy transition to renewables, nuclear and hydro in Africa, away first from coal, then oil and, in the second half of the century, from gas. Renewable energy production in Africa is in its infancy, and it will take several years to gain momentum and a decade or more to ramp up to levels at which renewables offer viable alternatives to fossil fuels. Hydro and nuclear projects must also ramp up rapidly.

The hydroelectric project with the most potential, the Grand Inga scheme in the DR Congo, now back on the table after many years, illustrates how new technologies could circumvent infrastructure constraints. Instead of the need for transmission networks to transport electricity to industry in Nigeria or South Africa, the project becomes commercially viable if it uses its vast electricity production to produce hydrogen at the source, then shipped to markets in Asia, Europe and elsewhere by sea.

In thinking about energy, African governments are primarily concerned about cost and speed and less about the choice of technology (nuclear or not). In this context, SMRs could significantly contribute to meeting Africa’s energy requirement in high-demand nodes. Rather than the development of traditional national electricity grids, baseload electricity supply needs to be taken to these nodes to create mini or smaller grids. Examples are the provision of energy for industrial or mining demand such as cement and fertiliser production, iron ore smelters, large data centres, and chemical and steel plants, much of which can be done using SMRs with project-specific additions from other energy sources to meet peaking demand. Africa will, however, not invest in technology demonstrators (first of kind) SMRs, implying that the most likely successful approach could either come later in the SMR development path (once demonstrator units are operating effectively elsewhere) or for SMR developers presenting a fleet option to several countries as a package option that resolves energy requirements across a host of higher demand nodes.

Africa has set a path towards industrialisation, regional trade, and integration. These two ambitions inevitably release more carbon than the other eight sectors modelled on this website and are included in the Sustainable Africa scenario. It is, therefore, important that industrial development, such as building fertiliser and cement plants, proceed with the appropriate technologies that keep carbon emissions to a minimum.

Given the fear of stranded assets, the inevitable question is: How and who will finance Africa’s ongoing fossil fuel exploration and production and for which market – for domestic consumption or export? Momentum is growing among wealthy countries to stop new investments in oil and gas ventures, and the risk of stranded investments is growing. Global demand for gas could change rapidly, which is important since much of Africa’s gas is for the more lucrative export market rather than domestic consumption. At the same time, Africa’s high levels of indebtedness and punitive risk premiums mean that the continent struggles to attract investment in the best circumstances. With an unreformed global financial system and capital mainly in the hands of the risk-averse private sector, the ability of African countries to borrow money at affordable interest rates is limited. At the same time, the large sums of money promised to help the green transition under the auspices of the so-called Just Energy Transition Partnerships have not materialised, and the result is that polluting coal plants stay open. Mozambique is an example of a country that has to enter into complex arrangements with private actors with only limited revenues flowing to the government towards the end of the project life cycle once the investors have recouped the return on their investment.

A previous section noted the extent to which revenue forecasts for oil and gas resources are regularly overstated, and today, these investments are considered even more risky. Oil and gas ventures often require several decades for governments to realise a reasonable return, underlining the fraught nature of these investments. Even if Africa were to get a reprieve on gas projects, the negative perceptions associated with investments in fossil fuels imply a high level of risk to private or public sector investors if the world were to pursue the UNEP production targets.

Africa would need lots of support from multilateral funding institutions, private sector partners, development agencies and bilateral support from high-income countries to realise a viable carbon emissions pathway, including for selected exploration and production of gas. The call is not new and was prominently made as part of the Bujumbura Declaration of August 2021 that urged the World Bank to scale up investments in energy cooperation in Africa, including the financing of gas-to-power projects beyond 2025. The obvious response would be to introduce a carbon tax on countries with high per capita emissions and those that have historically benefitted from a high carbon growth path, using the associated funds to fund Africa’s energy transition, as discussed in the theme on Africa’s Climate Futures. In addition to debt relief and suspension, multilateral development banks need to implement the Climate Resilient Debt Clauses (CRDCs) developed in response to the Sustainable Debt Coalition created at COP27 in Egypt and the use of debt-for-nature or debt-for-climate swaps to strengthen recipient countries, allowing them to repay their debts by investing in nature regeneration and climate action as recently proposed by the African Center for Economic Transformation. The recommendations are part of five financial proposals to help African countries finance a just and equitable climate transition at scale.[22]

The future carbon emissions from a handful of African countries are globally significant, namely Nigeria, Egypt, South Africa, Ethiopia, Algeria, the DR Congo, Mozambique, Tanzania, Uganda, Côte d’Ivoire, Morocco, Sudan and Zimbabwe. These are countries with rapidly growing populations and fossil fuel importers or producers. Their success in transitioning quickly to renewables and reducing their carbon footprint will be critical in determining Africa’s contribution to global warming and a sustainable global future.

Various estimates have been tabled about the cost associated with tripling renewables by 2030 (the target set at COP28), ranging from US$1.3 to US$2 trillion annually. According to Climate Analytics, investment in Africa needs to grow five-fold to ramp up renewables twice as fast as the global average. These are significant amounts, probably only available within the private sector in the developed world and through a carbon tax on high-income and high-carbon emitter countries to reduce emissions and fund the energy transition in regions such as Africa. Given the small contribution Africa and other areas have historically made to global carbon emissions, their current low emission levels and considerable developmental challenges, it is unlikely that developing countries would agree to a worldwide tax that does not recognise these inequities.

Africa needs vast amounts of energy. Linear, path dependency thinking is that the base load requirements cannot come from renewables given the variability of solar and wind. Unlike fossil fuels, conventional approaches constrain options for nuclear or hydro as they currently offer the required potential without a technological breakthrough with energy storage. Yet scaling up large-scale solar power in North Africa could power Europe, while the associated manufacturing requirements could significantly boost North Africa’s economies. Instead, Germany chose gas from Russia and closed its nuclear energy plants until the war in Ukraine ignited demand for gas from America instead of solar energy from the Sahara.

Without ‘out of the box thinking’, such as green hydrogen from Grand Inga and Namibia and bulk solar from the Sahara, the costs associated with hydro, hydrogen and nuclear energy, including the environmental challenges, appear to limit the feasibility of other options. In addition to wind, solar, geothermal, green hydrogen, and other renewables, Africans must explore local solutions, such as repurposing solid waste and making efforts towards a circular economy.